Many homeowners can't find their PMI on their mortgage statement. It can be listed under several names like "MIP/PMI," "Mortgage Insurance," or "MI Premium," and it's usually folded into your escrow payment alongside your taxes and homeowners insurance. Bundled in this way, many people never notice it and keep paying for years when they do not have to.

PMI hides in a few specific places on your statement. Here's exactly what to look for and where it usually appears.

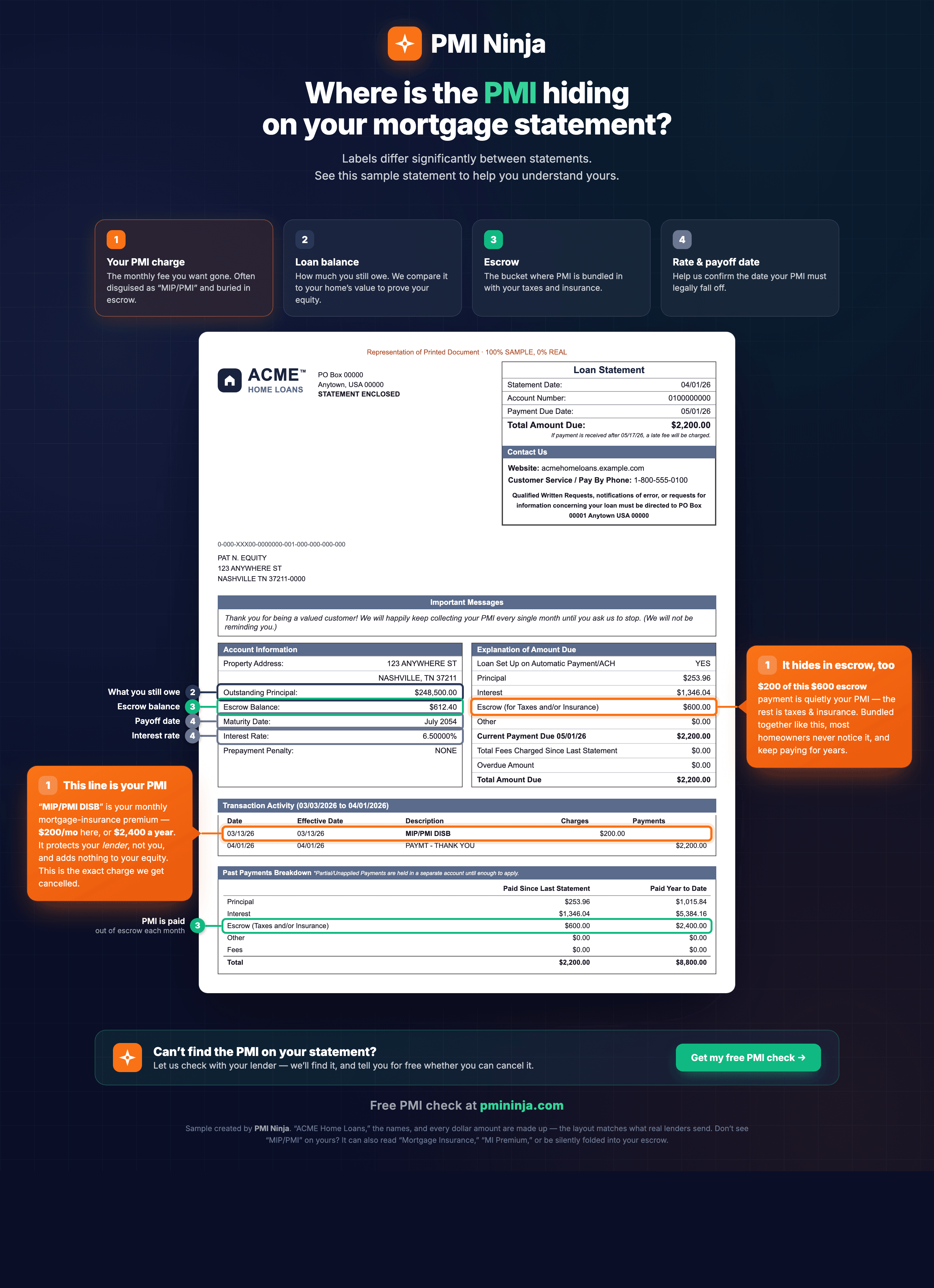

The four things to look for

- Your PMI charge — the monthly fee you want gone. Often shown as "MIP/PMI" and buried in your escrow activity.

- Loan balance — how much you still owe. We compare it against your home's value to prove your equity.

- Escrow — the bucket where PMI is bundled in with your taxes and insurance, which is why it's so easy to miss.

- Rate & payoff date — these help confirm the date your PMI must legally fall off.

In the sample above, the line reads "MIP/PMI DISB" at $200 a month — that's $2,400 a year. It protects your lender, not you, and adds nothing to your equity. On your statement it might instead read "Mortgage Insurance" or "MI Premium," or be silently folded into the escrow total with no separate line at all.

Can't find the PMI on your own statement? That's exactly what we check for free. We'll confirm with your lender whether you're paying it — and whether you can cancel it — at no cost and no obligation.

Ready to eliminate your PMI?

Two-minute check. No credit pull. We only get paid if your PMI is officially removed.